Introduction to FIFO

Inventory management plays a major role in business profitability and operational efficiency. One of the most widely used inventory accounting methods is FIFO, which stands for “First In, First Out.” Businesses across retail, manufacturing, food distribution, and warehousing rely on FIFO to manage inventory accurately and reduce waste.

Understanding how FIFO works can help companies improve cash flow, maintain accurate financial records, and make smarter business decisions. In this article, we will explain FIFO in simple terms, explore its benefits, provide practical examples and show how businesses use it every day.

What Does FIFO Mean?

FIFO stands for “First In, First Out.” It is an inventory valuation and accounting method where the oldest inventory items are sold or used first before newer inventory.

This approach assumes that products purchased or produced first are also the first ones to leave inventory. FIFO is especially useful for businesses dealing with perishable products or items that can become outdated over time.

For example, a grocery store selling milk will place older cartons at the front of the shelf so they are sold before newly stocked cartons. This is a practical application of FIFO.

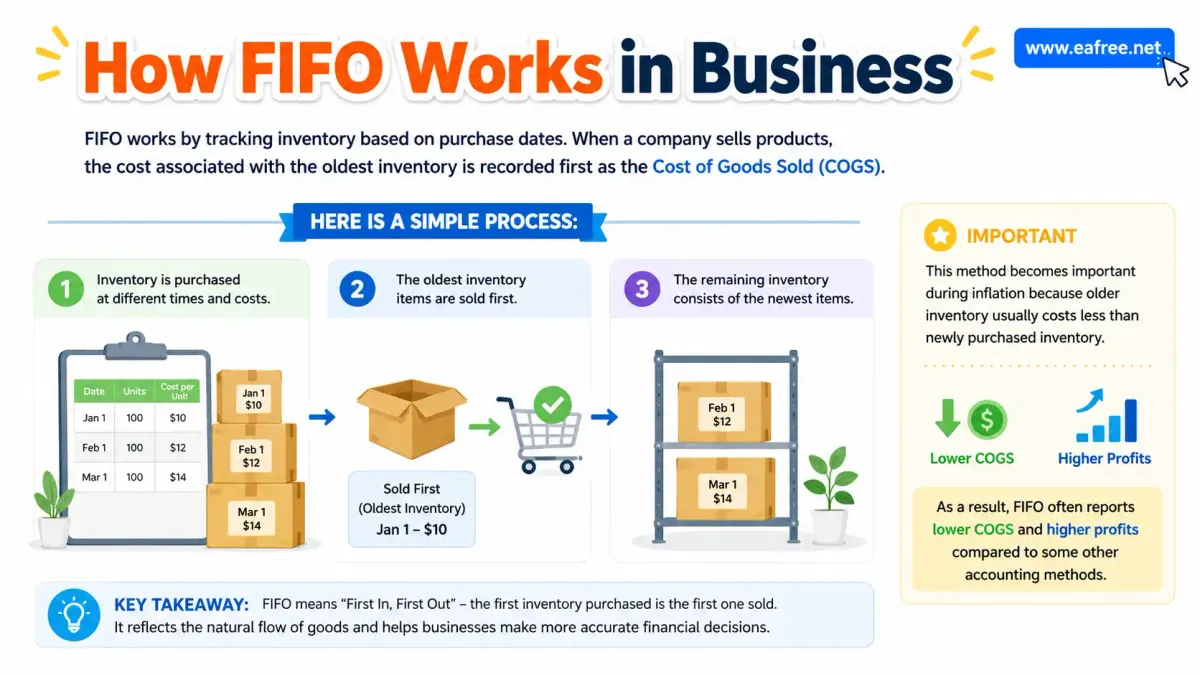

How FIFO Works in Business

FIFO works by tracking inventory based on purchase dates. When a company sells products, the cost associated with the oldest inventory is recorded first as the Cost of Goods Sold (COGS).

Here is a simple process:

- Inventory is purchased at different times and costs.

- The oldest inventory items are sold first.

- The remaining inventory consists of the newest items.

This method becomes important during inflation because older inventory usually costs less than newly purchased inventory. As a result, FIFO often reports lower COGS and higher profits compared to some other accounting methods.

//Example Workflow

| Date | Inventory Purchased | Cost Per Unit |

|---|---|---|

| Jan 1 | 100 units | $10 |

| Jan 15 | 100 units | $12 |

| Feb 1 | Sold 120 units | - |

Using FIFO:

- The first 100 units sold are valued at $10 each.

- The next 20 units sold are valued at $12 each.

COGS Calculation:

- (100 × $10) + (20 × $12) = $1,240

FIFO Formula and Calculation

The FIFO method does not use a complicated formula, but the calculation follows a logical sequence.

The general FIFO calculation is:

- Cost of oldest inventory is assigned to sold items first.

- Remaining inventory reflects the most recent purchase costs.

//FIFO Formula

Businesses often use accounting software to automate FIFO calculations, especially when handling large inventories.

FIFO is accepted under both International Financial Reporting Standards (IFRS) and Generally Accepted Accounting Principles (GAAP), making it one of the most trusted accounting methods worldwide.

Real-World FIFO Examples

Many businesses use FIFO daily without even realizing it. The method is common in industries where inventory freshness matters.

//Retail Stores

Clothing retailers sell older collections before introducing new seasonal products. This helps reduce unsold inventory and storage costs.

//Food and Beverage Industry

Restaurants and supermarkets use FIFO to prevent spoilage. Ingredients purchased earlier are used first to maintain product quality and food safety.

//Manufacturing Companies

Manufacturers use raw materials in the order they are received to avoid material deterioration and maintain production efficiency.

//Warehousing and Logistics

Warehouses organize inventory so older stock is shipped before newly arrived products. This minimizes product expiration and improves inventory turnover.

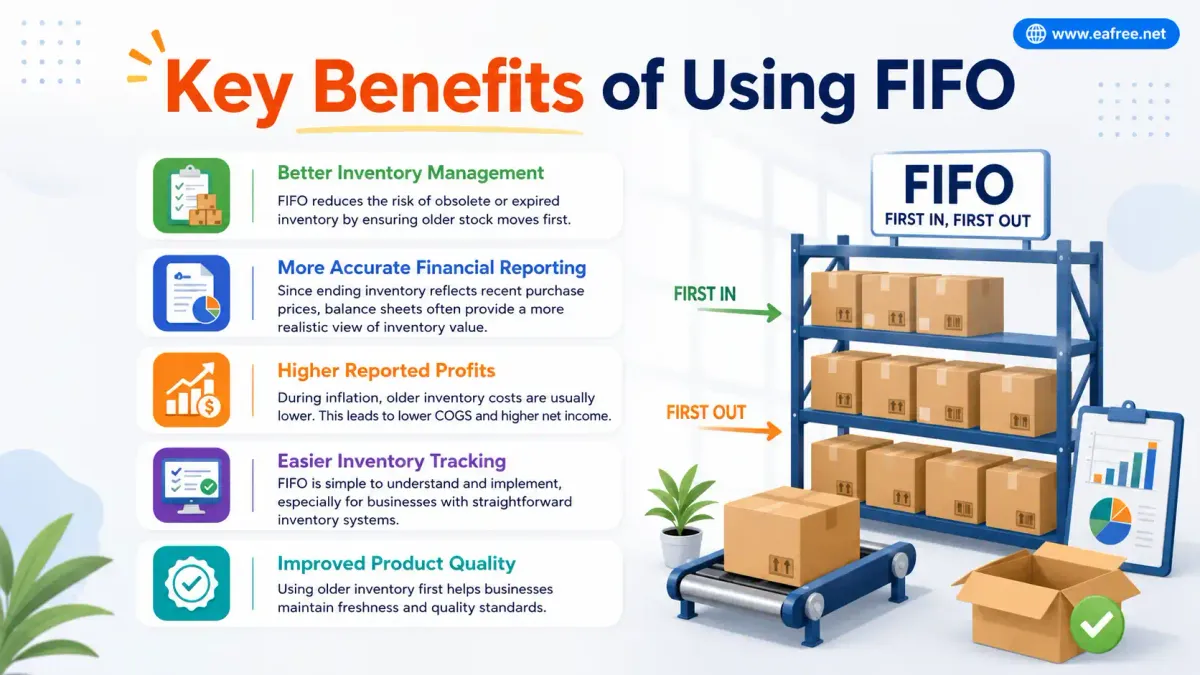

Key Benefits of Using FIFO

FIFO offers several advantages that make it attractive for businesses of all sizes.

//Better Inventory Management

FIFO reduces the risk of obsolete or expired inventory by ensuring older stock moves first.

//More Accurate Financial Reporting

Since ending inventory reflects recent purchase prices, balance sheets often provide a more realistic view of inventory value.

//Higher Reported Profits

During inflation, older inventory costs are usually lower. This leads to lower COGS and higher net income.

//Easier Inventory Tracking

FIFO is simple to understand and implement, especially for businesses with straightforward inventory systems.

//Improved Product Quality

Using older inventory first helps businesses maintain freshness and quality standards.

FIFO vs LIFO: What’s the Difference?

FIFO is often compared with LIFO, which stands for “Last In, First Out.”

Under LIFO, the newest inventory is sold first. This creates different financial outcomes.

| Feature | FIFO | LIFO |

|---|---|---|

| Inventory Sold First | Oldest inventory | Newest inventory |

| Ending Inventory Value | Higher during inflation | Lower during inflation |

| Reported Profit | Higher | Lower |

| Accepted Under IFRS | Yes | No |

| Best For | Perishable goods | Tax reduction strategies |

FIFO is generally preferred for businesses focused on accurate inventory valuation and operational efficiency.

Industries That Commonly Use FIFO

FIFO is widely adopted across many sectors because of its practical and financial advantages.

//Common Industries Using FIFO

- Retail and eCommerce

- Food and beverage

- Pharmaceuticals

- Cosmetics

- Manufacturing

- Electronics

- Warehousing and logistics

These industries often deal with products that can expire, lose value, or become outdated quickly.

Common Challenges of FIFO

Although FIFO has many benefits, businesses may face some challenges when using this method.

//Higher Tax Liability

Because FIFO often results in higher profits during inflation, companies may pay more taxes.

//Not Ideal for All Industries

Some industries with rapidly fluctuating costs may prefer other inventory methods for financial planning purposes.

//Requires Organized Inventory Systems

Businesses need accurate inventory tracking systems to apply FIFO correctly and avoid accounting errors.

Despite these challenges, FIFO remains one of the most commonly used inventory methods worldwide.

Best Practices for Implementing FIFO

Businesses can maximize FIFO efficiency by following a few best practices.

//Organize Inventory Properly

Arrange products so older stock is easier to access and sell first.

//Use Inventory Management Software

Automated systems help track inventory dates, quantities, and movement more accurately.

//Train Employees

Warehouse and retail staff should understand FIFO procedures to avoid stock rotation mistakes.

//Conduct Regular Inventory Audits

Frequent inventory checks help identify damaged, expired, or slow-moving products early.

Conclusion

FIFO is a simple yet highly effective inventory management and accounting method used by businesses around the world. By selling older inventory first, companies can reduce waste, improve product quality, and maintain more accurate financial reporting.

From grocery stores to manufacturing plants, FIFO helps businesses streamline operations and manage inventory more efficiently. Although it may lead to higher taxes during inflation, its simplicity and practical advantages make it a preferred choice for many organizations.

Understanding FIFO can help businesses make smarter financial decisions while improving operational performance and customer satisfaction.

FAQs

❓ What does FIFO stand for in accounting?

FIFO stands for “First In, First Out,” meaning the oldest inventory items are sold first.

❓ Why is FIFO important for businesses?

FIFO helps businesses reduce waste, improve inventory accuracy, and maintain product freshness.

❓ Is FIFO allowed under IFRS?

Yes, FIFO is accepted under both IFRS and GAAP accounting standards.

❓ Which industries benefit most from FIFO?

Industries dealing with perishable or fast-changing products, such as food, retail, and pharmaceuticals, benefit the most.

❓ What is the main disadvantage of FIFO?

During inflation, FIFO can result in higher profits and therefore higher tax obligations.