What Is Dollar-Cost Averaging (DCA)?

Dollar-Cost Averaging (DCA) is an investment strategy where you invest a fixed amount of money at regular intervals—regardless of the asset’s price. Instead of investing a large sum all at once, you spread your investments over time.

For example, instead of investing $12,000 in one go, you might invest $1,000 per month for 12 months.

The core idea behind DCA is simple:

- Buy more shares when prices are low.

- Buy fewer shares when prices are high.

- Reduce the impact of market volatility over time.

This strategy is commonly used in stock markets, mutual funds, ETFs and even cryptocurrencies.

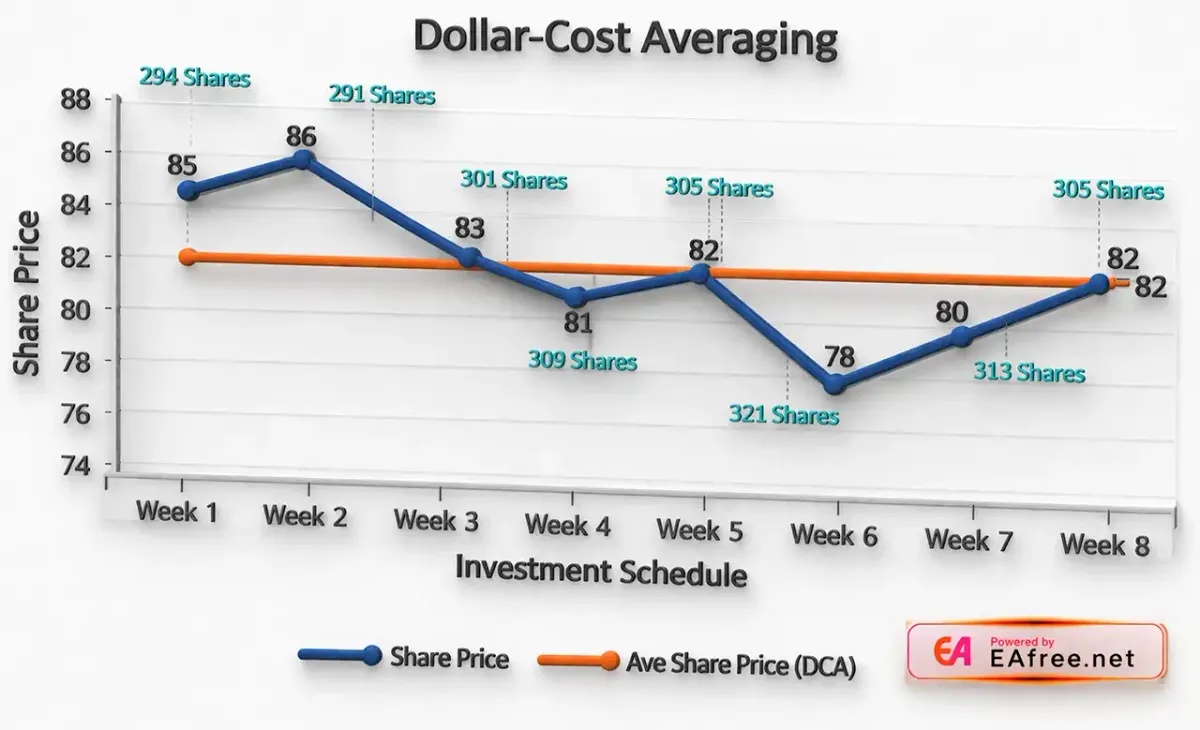

How Dollar-Cost Averaging Works

To understand DCA, let’s look at a simple example.

Imagine you invest $500 every month into a particular stock:

| Month | Price per Share | Amount Invested | Shares Purchased |

|---|---|---|---|

| Jan | $50 | $500 | 10 shares |

| Feb | $25 | $500 | 20 shares |

| Mar | $40 | $500 | 12.5 shares |

| Apr | $20 | $500 | 25 shares |

Over time, you accumulate shares at different price points. Your average cost per share becomes lower than if you had invested everything at a higher price.

This smoothing effect helps reduce the risk of investing at the wrong time.

Key Benefits of Dollar-Cost Averaging

//1. Reduces Market Timing Risk

One of the biggest challenges investors face is trying to predict market movements. Even experienced professionals struggle to consistently time the market correctly.

DCA removes this pressure by:

- Eliminating the need to guess market highs or lows

- Spreading risk across multiple entry points

This makes it especially useful for beginners or those who prefer a hands-off approach.

//2. Minimizes Emotional Investing

Emotions like fear and greed often lead to poor investment decisions. Investors may panic during downturns or become overly optimistic during market highs.

DCA encourages discipline by:

- Following a fixed investment schedule

- Avoiding impulsive decisions based on market news

Over time, this consistency can lead to better long-term outcomes.

//3. Makes Investing More Accessible

Not everyone has a large sum of money ready to invest. DCA allows individuals to start with smaller amounts and build wealth gradually.

Benefits include:

- Lower financial barrier to entry

- Easier budgeting and planning

- Suitable for regular income earners

//4. Takes Advantage of Market Volatility

Market volatility can be intimidating, but DCA turns it into an advantage.

When prices drop:

- Your fixed investment buys more shares

When prices rise:

- You still benefit from previous lower-cost purchases

This helps lower your average cost per unit over time.

//5. Encourages Long-Term Investing

DCA aligns well with long-term investment goals such as retirement or wealth accumulation.

By investing consistently:

- You stay focused on long-term growth

- You avoid short-term distractions

This approach is particularly effective in historically upward-trending markets.

Risks and Limitations of DCA

While DCA has many advantages, it’s not without drawbacks. Understanding the risks is crucial before adopting this strategy.

//1. Lower Returns in Strong Bull Markets

In a consistently rising market, investing a lump sum early may yield higher returns than spreading investments over time.

Why?

- Your money is fully invested from the beginning

- You benefit more from compounding

DCA may cause you to miss out on some potential gains in such scenarios.

//2. Requires Discipline and Patience

DCA is not a “get rich quick” strategy. It requires:

- Long-term commitment

- Consistent contributions

Investors who stop investing during downturns may lose the benefits of the strategy.

//3. Transaction Costs Can Add Up

Frequent investing may lead to:

- Higher transaction fees

- Increased brokerage costs

To minimize this risk, consider platforms with low or zero trading fees.

//4. Not a Complete Risk Elimination Strategy

DCA reduces timing risk, but it does not eliminate investment risk.

If the asset you invest in performs poorly over time:

- You may still incur losses

Therefore, asset selection remains critical.

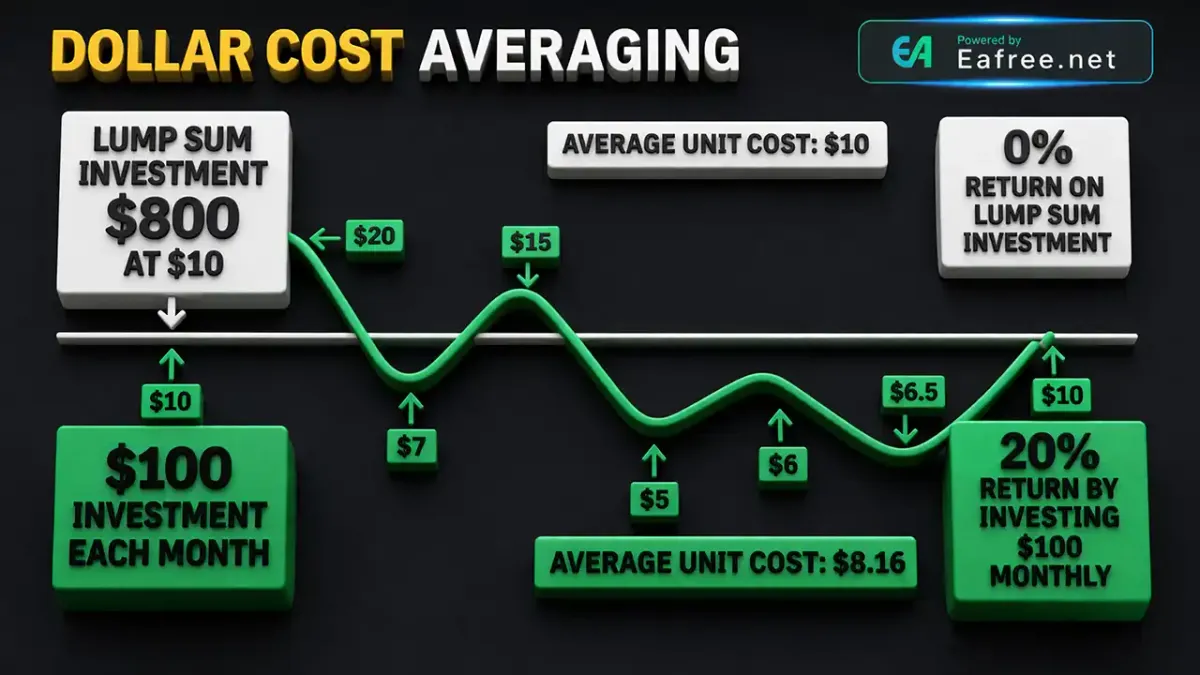

Dollar-Cost Averaging vs. Lump-Sum Investing

A common debate among investors is whether DCA is better than lump-sum investing.

//Lump-Sum Investing

- Invest all capital at once

- Potentially higher returns in rising markets

- Higher risk if market declines immediately

//Dollar-Cost Averaging

- Invest gradually over time

- Reduces timing risk

- More suitable for cautious investors

//Which One Is Better?

The answer depends on:

- Market conditions

- Risk tolerance

- Investment goals

Research suggests that lump-sum investing often outperforms DCA in the long run, but DCA provides psychological comfort and risk management.

When Should You Use Dollar-Cost Averaging?

DCA is particularly effective in the following situations:

//1. You Have a Regular Income

If you earn a steady paycheck, DCA allows you to invest consistently without needing a large upfront sum.

//2. You Want to Reduce Risk

DCA is ideal if you’re worried about investing at the wrong time or entering the market during volatility.

//3. You Are a Beginner Investor

For new investors, DCA provides a structured and less stressful way to start investing.

//4. You Are Investing in Volatile Assets

Assets like stocks or cryptocurrencies can fluctuate significantly. DCA helps smooth out these price swings.

How to Implement Dollar-Cost Averaging

Getting started with DCA is simple. Follow these steps:

//Step 1: Choose Your Investment

Select assets that align with your financial goals, such as:

- Index funds

- ETFs

- Stocks

- Cryptocurrencies

//Step 2: Decide Your Investment Amount

Determine how much you can invest regularly without affecting your financial stability.

//Step 3: Set a Schedule

Choose a consistent interval:

- Weekly

- Bi-weekly

- Monthly

Automation can help ensure consistency.

//Step 4: Stick to the Plan

The key to DCA success is discipline. Continue investing regardless of market conditions.

//Step 5: Monitor and Adjust

Periodically review your portfolio and adjust your strategy if needed, but avoid overreacting to short-term market changes.

Real-Life Example of DCA Success

Consider an investor who started investing monthly during a market downturn. While prices initially dropped, their consistent investments allowed them to accumulate shares at lower prices.

When the market eventually recovered:

- Their portfolio value increased significantly

- Their average cost remained lower than peak prices

This demonstrates how patience and consistency can pay off over time.

Common Mistakes to Avoid

Even with a solid strategy like DCA, investors can make mistakes:

- Stopping investments during market dips

- Investing in poor-quality assets

- Ignoring fees and expenses

- Lack of long-term perspective

Avoiding these pitfalls is essential for maximizing the benefits of DCA.

Is Dollar-Cost Averaging Right for You?

DCA is not a one-size-fits-all solution, but it is a highly effective strategy for many investors.

It may be right for you if:

- You prefer a low-stress investment approach.

- You want to build wealth gradually.

- You value consistency over timing.

However, if you have a large sum ready to invest and a high risk tolerance, lump-sum investing might be worth considering.

Final Thoughts

Dollar-Cost Averaging is a simple yet powerful strategy that helps investors navigate market uncertainty with confidence. By investing consistently over time, you reduce the impact of volatility, minimize emotional decision-making and build long-term wealth.

While it may not always deliver the highest possible returns, DCA provides something equally valuable: peace of mind and discipline.

In the end, the best investment strategy is the one you can stick with. And for many investors, Dollar-Cost Averaging offers exactly that.